Rear-ended car with damaged bumper at a city intersection after a collision with an uninsured driver

Uninsured Motorist Law: Your Rights and Compensation After an Accident

Content

Picture this: you're sitting at a red light when another car slams into you from behind. The other driver apologizes profusely but then admits they don't have insurance. Your stomach drops. Who's going to pay for the ambulance ride you're about to take? What about your totaled car sitting in the intersection?

Here's the uncomfortable truth—roughly one out of every eight drivers in America has no insurance whatsoever. That's about 13% of everyone sharing the highway with you during your morning commute. When someone without coverage causes your crash, you're suddenly facing a problem that most people don't discover until it's too late: their own insurance might be the only lifeline available.

Every state handles this differently. Some require you to have protection built into your policy. Others make it optional, and plenty of drivers have no idea whether they're covered or not. Understanding these protections before you need them makes the difference between recovering fully and spending years trying to collect money from someone who has nothing to give.

What Uninsured Motorist Coverage Actually Protects

Think of uninsured motorist coverage as insurance for when the other guy doesn't have insurance. You're basically paying your own carrier to step in when someone without coverage hurts you or damages your vehicle.

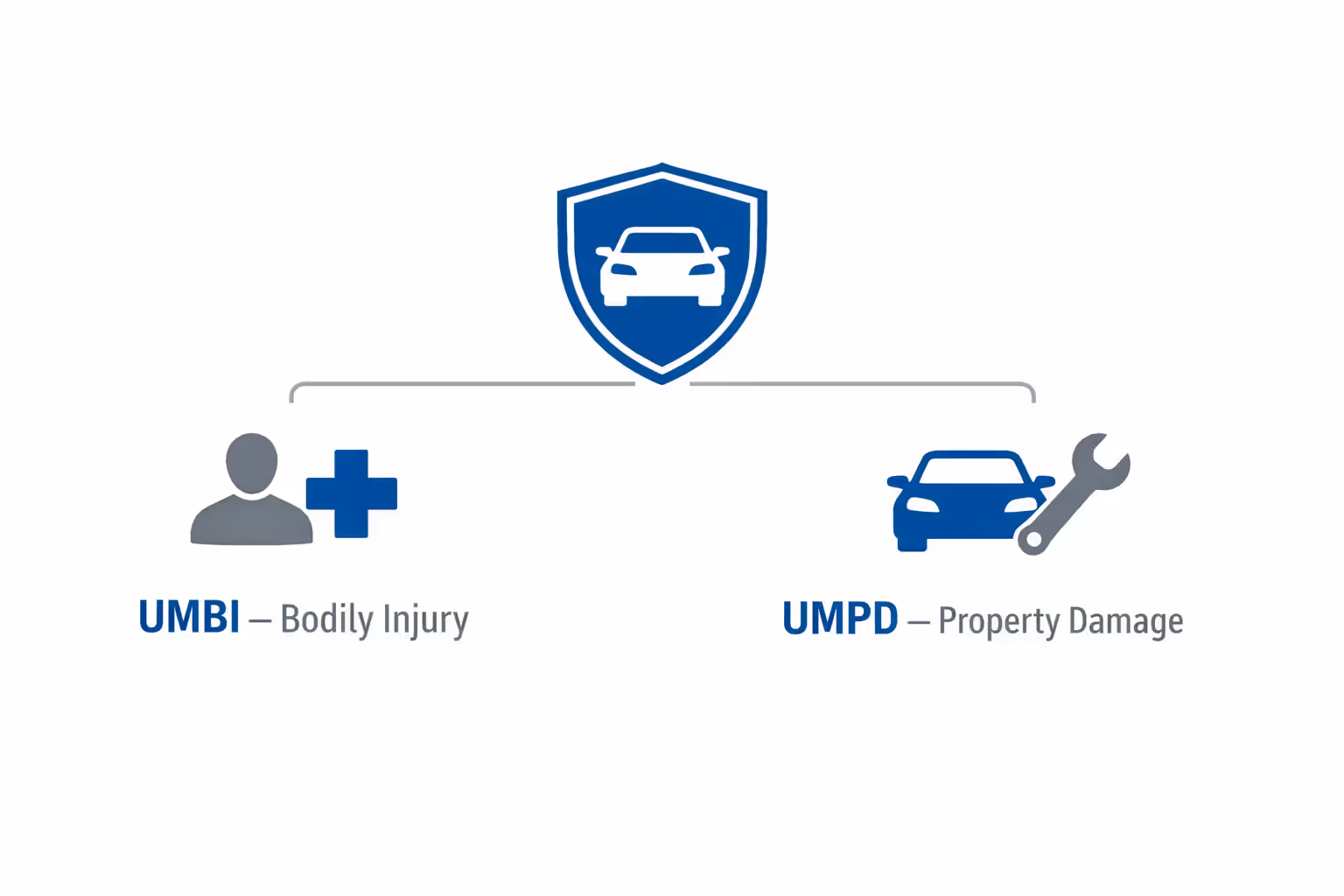

Most policies split this into two buckets. Bodily injury coverage (abbreviated as UMBI) handles everything related to physical harm—hospital bills, physical therapy, the paycheck you missed because you couldn't work, even compensation for ongoing pain. Property damage coverage (UMPD when available) takes care of your vehicle repairs and any personal items destroyed in the crash. Here's the catch: not every state requires insurers to offer both types, and some states fold property protection into your collision coverage instead.

Author: Marcus Delaney;

Source: capeverde-vip.com

What you can actually claim: - Every medical bill from the ER visit through months of follow-up appointments - Income you lost while recovering (salary, hourly wages, even missed overtime) - Physical therapy sessions and any specialized treatment - Money for lasting pain or permanent limitations on what you can do - Compensation for visible scars or disabilities - Vehicle repairs or replacement value (where UMPD exists)

What won't be covered: - Damage to someone else's property - Injuries to passengers riding with the uninsured driver - Your deductible in certain policy setups - Punitive damages in most cases - Anything beyond your policy's dollar limits

Here's how the math works. Let's say you bought $100,000 in UM protection. If your medical bills and lost wages add up to $75,000, your insurer cuts you a check for that full amount. But if your damages hit $150,000? You'll get your $100,000 maximum and need to figure out another way to collect the remaining $50,000.

Quick distinction here: underinsured motorist coverage (UIM) isn't quite the same thing. That kicks in when the at-fault driver has some insurance, but not enough. Imagine someone with just $25,000 in coverage causes an accident that leaves you with $80,000 in damages. Their carrier pays their limit of $25,000, then your UIM covers the additional $55,000 (assuming you purchased enough UIM coverage).

How State Laws Differ on Uninsured Driver Protection

The protection you have depends entirely on where your car's registered. Some states automatically include this coverage unless you specifically reject it in writing. Others treat it like an optional add-on that many drivers skip without understanding the risk.

| State | Mandatory/Optional | Minimum UM Limits | Can Reject Coverage? | Notes |

| California | Optional | $15K/$30K per accident | Yes, written refusal | Your insurer has to offer it; you sign to decline |

| Texas | Optional | Matches your liability limits | Yes, written refusal | Automatically offered at same level as liability unless declined |

| New York | Mandatory | $25K/$50K per accident | No | Every policy includes this automatically |

| Florida | Optional | No minimums set | Yes, written refusal | Insurers don't have to offer it |

| Illinois | Mandatory | $25K/$50K per accident | Limited circumstances | Written rejection allowed only in specific cases |

| Pennsylvania | Optional | $15K/$30K per accident | Yes, written refusal | Must be offered when you purchase policy |

| Ohio | Optional | $25K/$50K per accident | Yes, written refusal | Requires signed rejection form |

| Georgia | Optional | $25K/$50K per accident | Yes, written refusal | Must be presented; property damage handled separately |

| North Carolina | Mandatory | $30K/$60K per accident | Limited circumstances | Automatically included unless formally rejected |

| Michigan | Optional | Varies by insurer | Yes, written refusal | State's no-fault system affects how UM works |

| Virginia | Optional | $25K/$50K per accident | Yes, written refusal | Has one of the highest uninsured driver rates nationally |

| Washington | Optional | Varies by insurer | Yes, written refusal | Not required but must be offered as option |

| Massachusetts | Mandatory | $20K/$40K per accident | No | Included on every single policy |

| Arizona | Optional | Varies by insurer | Yes, written refusal | Must be offered at time of purchase |

| Tennessee | Optional | $25K/$50K per accident | Yes, written refusal | Requires written consent to decline |

States like Texas use a "mirror your liability" setup. Choose $100,000/$300,000 for liability? You'll automatically get offered the same limits for UM protection unless you turn it down. Better coverage, sure, but your premium goes up accordingly.

The mandatory states give you the strongest safety net. Get hit by an uninsured driver in New York or Massachusetts? You definitely have UM coverage available. In optional states—especially ones where insurers don't have to mention it—thousands of drivers are exposed without knowing it.

Some states also use different formulas called "reduced by" versus "excess" for underinsured claims. With "reduced by," if someone has $25,000 coverage and you have $100,000 UIM, you can collect up to $75,000 from your UIM (your limit minus what their insurance paid). In "excess" states, you might be able to claim up to your full $100,000 depending on total damages.

Filing a Claim After a Crash with an Uninsured Driver

Everything starts at the scene. The second you realize the other driver has no insurance, documentation becomes absolutely critical. Take photos of every dent and scratch on both vehicles from multiple angles. Photograph the broader scene—skid marks, traffic signals, road conditions. Get pictures of their license plate and driver's license if they'll allow it. Write down the names and phone numbers of anyone who saw what happened.

Call the police no matter how minor the crash seems. Officers will likely cite the uninsured driver, which creates an official government record proving they lacked coverage. In hit-and-runs where the other driver takes off, that police report becomes your primary evidence that an uninsured motorist was involved.

Contact your insurance company within 24 hours maximum. Every policy has language requiring "prompt" or "immediate" notification, and waiting too long can give them grounds to deny your claim entirely. When you call, be explicit: "I need to file an uninsured motorist claim." You'll be assigned an adjuster who opens your file and starts the investigation.

Build your documentation package: - The official accident report with case number - Medical records from every provider who treated you - Every medical bill, itemized with dates and amounts - Proof of missed work (pay stubs showing regular income, letter from your employer) - At least three repair estimates for your vehicle - Photos showing the progression of your injuries and all property damage - Written statements from witnesses (or their recorded accounts) - Your insurance policy showing what coverage you purchased

Write a detailed demand letter to your insurer spelling out every dollar you're claiming. Be specific here: list each medical expense with the date and provider, calculate your exact lost wages using your paystubs as proof, describe in detail how your injuries changed your daily life. The more concrete your demand, the stronger your negotiating position.

Simple UM claims with clear documentation and straightforward injuries typically close in 30 to 90 days. Complicated cases involving permanent disabilities or disputes about who was at fault can drag on for six months to over a year.

The single biggest mistake I see accident victims make is treating their own insurance company like an ally. In an uninsured motorist claim, your insurer is the one writing the check — and they have every incentive to minimize what they pay. Document relentlessly, never give casual recorded statements, and understand that the burden of proving your damages falls entirely on you

— Robert Hunter

Common Mistakes That Delay or Deny Your Claim

Waiting to see a doctor causes more claim denials than almost anything else. Adjusters assume that if you didn't need immediate treatment, you weren't really hurt. Even if you feel only slightly sore, get examined within 24 hours. Injuries like whiplash often don't produce symptoms until the next day or even later.

Giving recorded statements without thinking them through creates problems. Your insurer will probably ask for a recorded statement, which your policy might require. But offhand comments like "I'm doing fine" or "It could be worse" get used against you later to argue your injuries weren't serious. Stick to facts: what happened, where the impact occurred, what symptoms you've noticed. Don't guess about fault or minimize how you feel.

Author: Marcus Delaney;

Source: capeverde-vip.com

Accepting the first settlement offer almost always means leaving money behind. Initial offers typically lowball your claim, particularly the non-economic stuff like pain and suffering. Don't even consider settling until you've finished treatment and understand the full extent of your injuries.

Throwing away evidence causes headaches down the line. Keep damaged clothing or personal items. Write daily notes about how your injuries affect simple tasks. Save every receipt connected to the accident—even parking fees for doctor appointments or money you paid someone to mow your lawn because you couldn't do it yourself.

Social media posts can torpedo your case. Adjusters routinely check Facebook and Instagram. One photo of you smiling at a family gathering can be twisted into "proof" you're not injured, even if you were in significant pain the whole time. Make your profiles private and don't post anything about the accident or your activities until your claim is completely resolved.

When Your Own Insurance Company Disputes Your Claim

Here's what catches people off guard: your own insurance company isn't necessarily on your side with UM claims. You're filing against your own policy, which means they're paying out of their own pocket. This creates tension where your insurer might challenge whether the other driver was really uninsured, question how badly you're hurt, or dispute what your damages are worth.

Common disputes include: - Claiming the other driver actually had insurance (maybe expired or cancelled, but they argue it was active) - Saying you were partially at fault, which reduces your recovery under comparative negligence rules - Arguing your injuries existed before this accident - Questioning whether your medical treatment was necessary - Challenging your vehicle's value or repair costs

When disputes pop up, fight back with documentation. If they say the other driver had insurance, get a formal denial letter from that insurance company. If they question medical necessity, get your doctor to write a letter explaining why each treatment was appropriate. For property damage disagreements, pay for an independent appraiser.

Most UM policies include arbitration clauses requiring disputes to go through binding arbitration instead of court. An arbitrator—usually a former judge or experienced attorney—hears both sides and makes a decision. This is typically faster and cheaper than a lawsuit, though you give up your right to a jury trial.

If your insurer acts in bad faith—unreasonably delaying your claim, denying coverage without legitimate grounds, or failing to properly investigate—you might have grounds to sue them for bad faith. These cases are tough to win but can result in damages far exceeding your policy limits, plus punitive damages.

Legal Options When Insurance Coverage Gaps Leave You Short

When UM coverage doesn't fully cover your losses, you face tough choices. The most obvious option is suing the uninsured driver personally, though this often proves pointless. People who can't afford insurance rarely have assets you can seize to satisfy a judgment. You might win a $100,000 court judgment against someone with no savings, no home, and a minimum-wage job.

Before suing someone personally, investigate their financial situation. Do they have a steady job with garnishable wages? Do they own property? Even if they're currently broke, financial situations change. Judgments typically stay enforceable for 10-20 years depending on your state and can often be renewed. Someone with nothing today might have assets worth pursuing in five years.

Wage garnishment lets you collect a portion of the debtor's paycheck (usually 25% of disposable income or the amount by which weekly wages exceed 30 times minimum wage, whichever is less). This only works if they maintain steady employment earning above minimum wage.

Author: Marcus Delaney;

Source: capeverde-vip.com

Property liens attach to any real estate the defendant owns now or buys later. If they own a house, your lien must be paid when they sell or refinance. If they don't currently own property, the lien attaches to anything they purchase in the future.

Asset searches conducted by specialized firms can uncover hidden bank accounts, investments, or business interests. These searches cost a few hundred dollars but might reveal assets that make pursuing the case worthwhile.

Look into stacking coverage from multiple policies. If you were injured while driving someone else's vehicle, you might be able to claim under both that vehicle's policy and your own personal auto policy. Some states allow "stacking," where you combine limits from multiple policies. If you own three vehicles each with $50,000 UM coverage, stacking could give you $150,000 in total protection.

Most accident victims assume that once their uninsured motorist coverage runs out, they're out of options. That's not always true. When damages are substantial, spending an hour with an attorney can reveal whether the at-fault party has assets worth pursuing, whether additional insurance policies might apply, or whether third parties share some liability. I've handled cases where a bar that overserved an obviously drunk patron or a repair shop that did negligent work became the actual source of recovery

— Jennifer Martinez

Third-party liability sometimes opens unexpected doors. If the uninsured driver was working when the accident happened, their employer might be liable under respondeat superior doctrine. If mechanical failure contributed, the manufacturer or repair shop might share responsibility. If the driver was drunk, the bar or person who provided the alcohol might face dram shop liability.

MedPay coverage on your own policy provides another layer. Medical payments coverage pays medical expenses regardless of who caused the accident, up to your policy limits (usually $1,000-$10,000). This coverage pays in addition to UM benefits and doesn't require proving fault.

Your health insurance becomes crucial when auto coverage falls short. Your health insurer pays medical bills subject to your deductible and copays. However, health insurers typically assert subrogation rights—if you later recover money, you might have to reimburse them for what they paid. Negotiate these liens aggressively, as health insurers often accept significantly reduced reimbursement.

Special Considerations for Commercial and Trucking Accidents

Commercial vehicle crashes add layers of complexity absent from regular car accidents. When an uninsured commercial truck or delivery vehicle hits you, multiple parties might be liable even when the driver personally has no insurance.

Trucking companies must maintain minimum federal insurance: $750,000 for most trucks, $1 million for hazmat carriers, and $5 million for certain dangerous cargo. However, owner-operators leasing their trucks sometimes let coverage lapse. Independent contractors operating outside federal oversight might carry minimal or zero coverage.

When investigating compensation options after a trucking crash, identify every potentially liable party: - The driver themselves - The trucking company that employs or contracts with them - The entity that owns the truck (if different from who operates it) - The shipper or cargo owner - Maintenance facilities if mechanical failure contributed - Manufacturers if defective parts caused the crash

Motor carrier liability often provides recovery even when drivers lack personal insurance. Trucking companies are liable for employee negligence under respondeat superior principles. Even when drivers work as independent contractors, companies might be liable if they negligently hired someone unqualified, failed to verify insurance status, or inadequately supervised them.

Check the FMCSA's SAFER database to verify a trucking company's insurance status and safety record. This free government database shows active insurance policies, safety ratings, and inspection results. If the database shows no active insurance for the carrier, you've got official documentation of uninsured status.

In commercial trucking cases, the driver behind the wheel is rarely the only responsible party. Carriers, brokers, shippers, and maintenance providers all have legal duties — and often carry substantial insurance. Identifying every link in that chain of liability is what separates a modest settlement from full compensation for a catastrophically injured victim

— J. Andrew Meyer

Non-trucking liability insurance (sometimes called bobtail insurance) covers owner-operators when driving without cargo or outside dispatch. If the trucker who hit you was driving home after finishing a delivery, their non-trucking policy might provide coverage even if their primary commercial policy had lapsed.

Cargo insurance sometimes extends liability coverage. If the crash happened while hauling freight, the shipper's insurance might provide additional coverage layers.

Corporate structure investigations can reveal assets beyond individual drivers. Trucking companies might operate as LLCs or corporations with substantial assets. Even if the driver personally has nothing, the company might have significant resources or active insurance covering the incident.

Freight brokers face growing liability exposure. Courts increasingly hold brokers responsible for negligently selecting carriers with poor safety records or inadequate insurance. If a broker hired an uninsured carrier with a history of violations, the broker might share liability.

Calculating What You Can Recover from an Uninsured Motorist Claim

Author: Marcus Delaney;

Source: capeverde-vip.com

UM claims compensate both economic and non-economic damages, subject to your policy limits. Understanding what you can recover helps you evaluate settlement offers and decide whether additional legal action makes sense.

Economic damages include all quantifiable financial losses:

Medical expenses cover everything injury-related: ER visits, ambulance transport, hospital stays, surgeries, medications, physical therapy, chiropractic care, counseling for accident-related trauma, and future medical care for permanent injuries. Keep itemized bills showing dates, providers, and amounts. For ongoing treatment, get your doctor's written opinion on future medical needs and projected costs.

Lost income includes earnings you couldn't generate due to injuries. This covers salary, hourly pay, commissions, bonuses, and self-employment income. Document losses using pay stubs showing your normal earnings, employer letters confirming missed work, and tax returns for self-employed individuals. If injuries cause permanent disability preventing you from returning to your previous job, you can claim lost future earning capacity—the difference between what you would have earned and what you can now earn.

Property damage addresses vehicle repair or fair market replacement value, plus damaged personal property like phones, laptops, or clothing. In states where UMPD coverage exists, this comes from your UM policy. In states without UMPD, you'll need collision coverage or must pursue the at-fault driver personally for property losses.

Out-of-pocket expenses capture accident-related costs like rental cars, transportation to medical appointments, household services you hired because you couldn't perform them yourself, and modifications to your home or vehicle to accommodate disabilities.

Non-economic damages compensate intangible losses:

Pain and suffering represents physical discomfort and ongoing pain from injuries. There's no precise formula, but insurers often use multipliers: multiply economic damages by 1.5 to 5 depending on severity. A minor soft tissue injury might warrant a 1.5-2x multiplier, while permanent disability might justify 4-5x.

Emotional distress covers psychological impacts: anxiety, depression, PTSD, fear of driving, or sleep problems. Documentation from mental health providers strengthens these claims substantially.

Loss of enjoyment concerns your inability to participate in activities you previously enjoyed. If you can no longer play with your kids physically, pursue hobbies, or engage in sports, you're entitled to compensation.

Loss of consortium compensates your spouse for lost companionship, affection, and intimacy due to your injuries.

| Damage Category | Coverage Details | Limit Structure | Realistic Example |

| Medical Bills | All injury-related treatment, both current and future care | Your UM policy maximum applies | $45,000 covering ER visit, surgery, and six months of physical therapy |

| Lost Income | Wages missed during recovery period | Subject to UM policy ceiling | $12,000 for three months unable to work full-time |

| Diminished Earning Capacity | Reduced future earnings from permanent disability | Capped by UM policy limit | $200,000 representing lifetime reduced earning power |

| Property Loss | Vehicle repair or replacement, damaged belongings | UMPD limit or collision coverage | $8,500 for repairs, $500 for destroyed laptop |

| Pain & Discomfort | Physical suffering, chronic pain | Typically 1.5-5x economic damages | $85,000 for permanent back injury (1.5x multiplier on $57,000 in hard costs) |

| Psychological Harm | Mental trauma, anxiety, depression | Varies; requires professional documentation | $15,000 covering PTSD counseling and ongoing anxiety treatment |

| Spouse's Loss | Partner's loss of companionship and intimacy | State-specific | $25,000 for spouse's lost companionship from permanent injury |

Punitive damages rarely appear in UM claims. These punish outrageous behavior rather than compensating actual losses. A few states allow punitive damages in UM claims if the uninsured driver's conduct was egregious (severe intoxication, intentional acts), but many prohibit punitive damages against your own insurer in UM claims.

Policy limits cap your total recovery. With $50,000 in UM coverage but $150,000 in damages, your UM claim maxes out at $50,000. This is why purchasing high UM limits is so important—they're relatively cheap compared to the protection they provide.

Comparative negligence reduces recovery if you share fault. If you're found 20% at fault for the crash, your recovery drops by 20%. In some states, being 50% or more at fault bars recovery entirely.

Frequently Asked Questions About Uninsured Motorist Law

An accident with an uninsured driver doesn't mean you're out of options. Uninsured motorist coverage provides the primary line of defense, covering injuries and sometimes property damage up to your policy limits. When coverage falls short, legal action against the at-fault driver, third parties, or through supplemental insurance policies might bridge the gap.

The key is acting quickly and strategically. Document everything at the scene, notify your insurer immediately, and preserve all evidence of damages. Understand exactly what your UM coverage includes and excludes. Don't accept quick settlement offers without fully understanding your injuries and their lasting impact.

For serious injuries or complicated situations—especially commercial vehicle crashes or cases where damages exceed your UM limits—consulting an attorney protects your interests. Many personal injury lawyers work on contingency, charging fees only if you recover money, making legal help accessible even when facing financial stress from an accident.

The most important decision happens before any crash occurs: carrying adequate uninsured motorist coverage. With roughly one in eight drivers operating without insurance, UM coverage isn't optional protection for unlikely scenarios—it's essential coverage for a common risk. Review your policy today, and if your UM limits seem low or nonexistent, increase them. The modest premium increase provides protection worth exponentially more than its cost.